July 26, 2024

2Q2024’s earnings surpassed full-year 2023’s

Ho Chi Minh City, 26 July 2024 – Masan Group Corporation (HOSE: MSN, “Masan” or the “Company”), today released its unaudited management accounts for the second quarter (“2Q2024”).

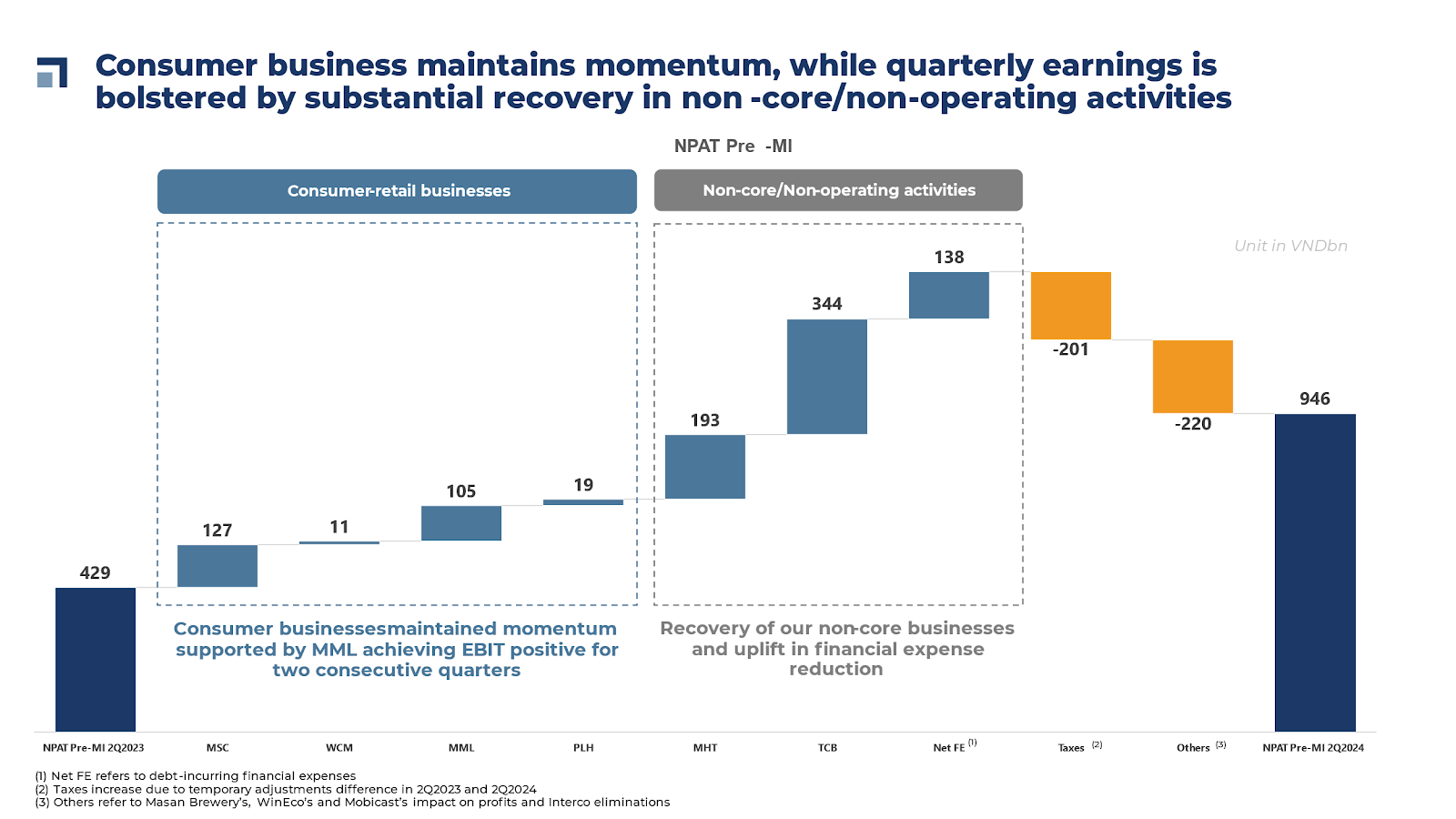

- Consumer-retail businesses1 maintained growth momentum, further supported by non-core business units profit uplift.

- Masan Consumer Corporation2 (“MSC”) delivered 14.0% YoY revenue growth in 2Q2024 to VND7,387 billion, driven by Convenience Foods (+20.7% YoY), Beverages (+17.6% YoY), and Coffee (+16.0% YoY). MSC maintained gross margin at a relatively high level of 46.3%, driven by power brands and premiumization acceleration commanding pricing power in the context of lower raw material costs. NPAT Pre-MI margin recorded 24.2%.

- WinCommerce (“WCM”) reported 9.2% YoY revenue growth in 2Q2024 to reach revenue of VND7,844 billion across the whole network, mainly driven by new store formats of WIN (catering to urban shoppers) and Winmart+ Rural (catering to rural shoppers), with 6.3% and 10.7% LFL YoY growth, respectively. LFL growth accelerated to 6.8% in 2Q2024 and to 9.7% in June, primarily driven by an increase in traffic. WCM reported NPAT-positive in June 2024, providing a clear pathway to sustainable profitability.

- As of June 2024, WCM operated 3,673 WCM stores, a net opening of 40 new stores since December 2023 as management exercised prudence amidst uncertainty in operating environment. WCM expects to accelerate store openings in 2H2024.

- In 2Q2024, WCM recorded VND172 billion in EBITDA, up 11.1% YoY. Excluding the one-off profit from financial product distribution pilot in 2023, EBITDA increased by 33% YoY.

- Masan MEATLife (“MML”) delivered VND105 billion YoY uplift in EBIT in 2Q2024, reporting the second consecutive quarter of EBIT-positive, driven by increased sales mix from processed meat while benefiting from higher chicken and pork market prices and declining feed costs. MML continues its mission to revolutionize the under-developed Vietnamese processed meat market with tasty, healthy, high quality, non-additive products, with the two Love Brands Ponnie and Heo Cao Boi having captured ~50% of the respective market share in the sterilized sausage market.

- Phuc Long Heritage (“PLH”)’s net revenue grew by 5.3% YoY to VND391 billion in 2Q2024, mainly driven by contribution from 15 new stores opened since 2Q2023. Management continued to maintain a prudent approach with 4 new stores outside of WCM added to the network in 2Q2024, now standing at 163 stores nationwide. LFL daily sales of PLH stores outside of WCM increased by 2.4% from the trough in 4Q2023, signaling recovering domestic demand for food services.

- Masan High-Tech Materials (“MHT”)’s EBIT improved by VND193 billion, supported by increasing APT and copper prices. The sale of H.C. Starck Holding GmbH to Mitsubishi Materials Corporation for an equity purchase price of USD134.5 million is expected to close before year-end 2024, upon which MHT is expected to book a one-time profit gain of approximately USD40 million in 2H2024 and benefits from long-term NPAT uplift of USD20-30 million. Transaction proceeds will be used to reduce MHT’s outstanding debt balance, whilst the deconsolidation of HCS also means MHT is relieved from HCS’s pension liabilities of approximately USD190 million as of 2Q2024.

- Techcombank (“TCB”), Masan’s associated company, contributed VND1,236 billion in EBITDA in 2Q2024, representing 38.5% YoY growth. For detailed results, please refer to the bank’s website.

Consolidated Financial Results:

- Net Revenue: In 2Q2024, Masan Group’s net revenue reached VND20,134 billion, a 8.2% increase from VND18,609 billion in 2Q2023, driven by robust topline performance in core consumer-retail businesses.

- EBITDA: EBITDA reached VND3,823 billion in 2Q2024, increasing by 20.9% YoY. This significant uplift was driven by the recovery of TCB and MHT. Meanwhile, all core consumer-retail businesses maintained positive earnings growth momentum.

- Net Profit After Tax (“NPAT”): NPAT Post-MI of VND503 billion in 2Q2024 is up 378.6% YoY, surpassing FY2023 NPAT Post-MI of VND419 billion, driven by improvements across consumer – retail businesses, the recovery of non-core/non-operating activities in 2Q2023, and VND138 billion lower in debt-incurring net financial expenses.

- Balance Sheet Highlights:

- Cash and cash equivalent balance increased to VND21,977 billion as of 2Q2024, compared to VND16,919 billion as of 4Q2023 as a result of improvement in free cash flows and cash injection from corporate funding activities.

- Net debt / LTM (last 12 months) EBITDA declined to 3.3x, compared to 3.9x as of 4Q2023, achieving the target of Net Debt to EBITDA below 3.5x.

- LTM Free cash flow (“FCF”) increased to VND7,429 billion as of 2Q2024, up 71% YoY.

2H2024 Guidance:

Strategic pillars:

- Continued focus on profitable growth driven by core consumer businesses.

- WIN Membership to create value for Masan’s businesses and partner brands.

- Further deleverage to improve balance sheet and reduce financial expenses.

- Reduce interest in non-core businesses while maintaining stringent capital allocation strategy.

- MSC: Accelerate topline growth in 2H2024 by continuing to execute premiumization and innovation strategy while streamlining underperforming SKUs to optimize profitability.

- WCM: Continue to focus on achieving NPAT breakeven by accelerating LFL growth to 8-9% YoY while enhancing store opening pace to achieve ~100 new stores per quarter. WCM will continue to strengthen the grip in rural areas with Rural minimart format.

- MML: Further invest in long-term profit driver of processed meat to achieve sustainable profitability.

- PLH: Improve LFL growth and join WIN Membership coalition to further enhance profit margin.

- MHT: Close the sale of HCS to de-lever and record one-off income while continuing to execute on cost optimization and operational efficiency improvements.

1 Consumer-retail businesses refer to MSC, WCM, MML and PLH

2 Masan Consumer Corporation is currently listed on the UPCoM stock exchange and does not include the beer business Masan Brewery